Estimated reading time: 5 minutes

The tax benefits of an IRA are not a right — they’re a privilege.

And like any privilege, they can be lost if misused, especially if you commit a prohibited transaction.

Prohibited transactions can jeopardize the tax-advantaged status of your self-directed IRA (SDIRA), leading to hefty penalties and potential disqualification of the account.

In this article, we’ll break down five of the most common prohibited transactions and share practical tips on how to avoid them, helping you to safeguard your SDIRA’s tax-advantaged status.

Table of Contents

- The Purpose of IRAs

- What is a Prohibited Transaction?

- Consequences of Engaging in Prohibited Transactions

- 5 Common Prohibited Transactions

- How to Avoid Prohibited Transactions

- Self-Directed IRA Prohibited Transaction FAQs

- Learn More About Self-Directed IRA Prohibited Transactions

The Purpose of IRAs

Congress created IRAs in 1974 to encourage people to save for retirement by offering significant tax advantages. These tax advantages are offered with the expectation that IRAs will be used strictly for retirement savings and not for personal benefit or gain.

To safeguard this intent, the IRS has established strict rules against certain activities, including prohibited transactions.

What is a Prohibited Transaction?

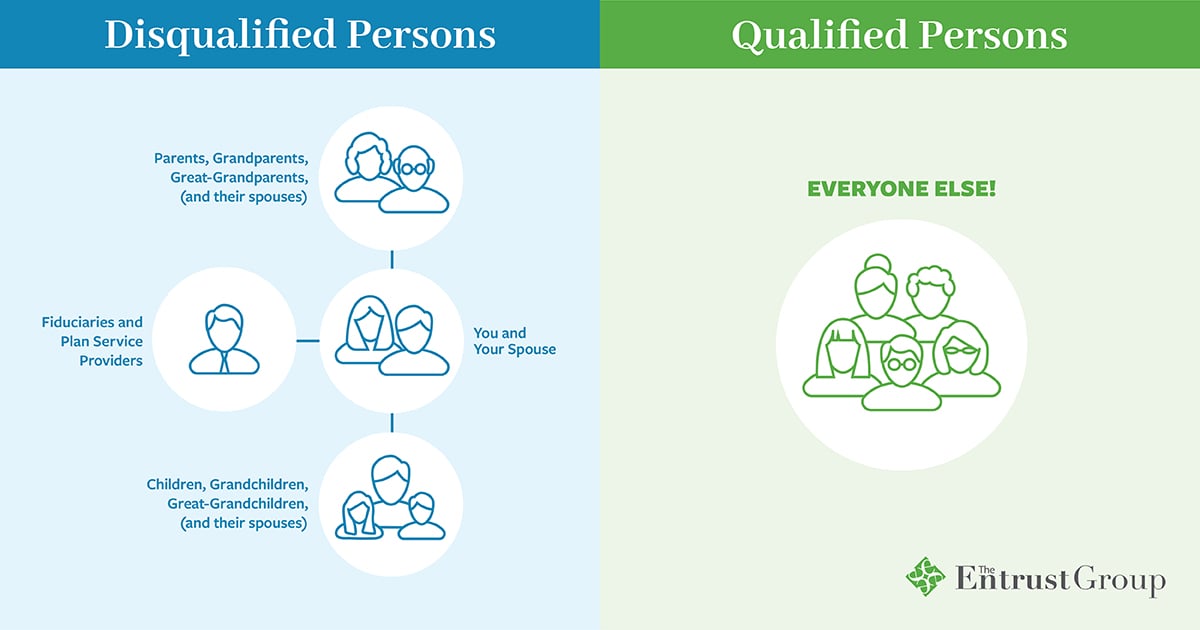

A prohibited transaction is any improper use of your IRA by you, your beneficiary, or any disqualified person.

Disqualified persons include the IRA owner, certain family members (including one’s spouse, lineal ascendants, descendants, and their spouses), and any entities in which the IRA owner has a significant ownership interest.

These transactions typically involve conflicts of interest or self-dealing, where the IRA owner or other disqualified persons directly or indirectly benefit from the IRA assets. According to the Internal Revenue Code (IRC) Section 4975, prohibited transactions include, but are not limited to:

- Sale, exchange, or leasing of property between the IRA and a disqualified person

- Lending money or other extension of credit between the IRA and a disqualified person

- Furnishing goods, services, or facilities between the IRA and a disqualified person

- Transfer to, or use by or for the benefit of, a disqualified person of any IRA income or assets

- Dealing with income or assets of the IRA by a fiduciary in their own interest or for their own account

Consequences of Engaging in Prohibited Transactions

Engaging in prohibited transactions can bring severe consequences, including:

Immediate Disqualification of the IRA

If your SDIRA engages in a prohibited transaction, it may be disqualified as of the first day of the year in which the transaction occurred.

For example, if you committed a prohibited transaction on October 10, 2025, the entire account would be considered distributed on January 1, 2025. This means that the tax-advantaged status of your IRA is lost, and the entire value of the IRA becomes taxable.

Potential Hefty Tax and Penalties

If any of the funds in the IRA are tax-deferred, the tax-deferred amount is immediately subject to federal and state income tax. If you are under the age of 59½ and do not meet one of the distribution exceptions, you may also incur a 10% early withdrawal penalty.

Additional Excise Tax for Disqualified Persons

If any disqualified person engaged in the prohibited transaction, they must pay an initial 15% excise tax of the total value involved in the transaction. This tax applies for each year (or part of the year) during the “taxable period,” which refers to the time between when the transaction took place and when it was corrected.

If the disqualified person fails to correct the prohibited transaction during this taxable period, an additional 100% tax is imposed on the amount involved. This tax must be paid by any disqualified person who participated in the prohibited transaction.

5 Common Prohibited Transactions

To maintain the tax-advantaged status of your IRA, it’s crucial to avoid these five common prohibited transactions:

1. Buying from or Selling to Disqualified Persons

One of the most frequent violations involves buying assets from or selling assets to disqualified persons.

For instance, if your IRA buys a rental property from your personal funds, this would be considered a prohibited transaction. Selling property owned by your IRA to your son-in-law would also violate the rules.

2. Personal Use of IRA Assets

Any personal benefit from SDIRA assets is strictly prohibited. Assets held in the SDIRA are for investment purposes only, with no personal use until retirement distributions.

For example, you cannot use an SDIRA-owned vacation property for personal vacations, even if you pay market rent. Storing your personal items in an SDIRA-owned facility would also be prohibited.

3. Providing Services to IRA-Owned Properties

Personally performing services, such as maintenance or management, to properties owned by your SDIRA is considered self-dealing.

If your SDIRA owns a rental property, you cannot perform repairs like fixing a leaky roof or painting the walls. Even mowing the lawn would be considered providing a service to the investment property.

4. Lending Money to Disqualified Persons

Your SDIRA cannot provide loans to disqualified persons, including yourself, your spouse, close family members, or any business entities you control.

5. Using IRA as Security for a Loan

Using IRA assets as collateral for personal loans is strictly prohibited by the IRS to ensure IRA funds are strictly for investment purposes.

How to Avoid Prohibited Transactions

Here are some strategies to avoid prohibited transactions, maintain compliance, and protect the tax-advantaged status of your IRA:

1. Invest Time in Your Education

“An investment in knowledge pays the best interest.” — Benjamin Franklin

Educate yourself on the rules governing SDIRAs, especially IRS guidelines around prohibited transactions. Knowing what constitutes a prohibited transaction, such as self-dealing or involving disqualified persons, is crucial to safeguarding your IRA. IRS Publication 590 provides a comprehensive overview of what is allowed and what is not.

For a more reader-friendly breakdown of the IRS rules, download our SDIRA Rules Guide. And consider keeping up-to-date with the new IRS rules and guidelines by subscribing to our monthly newsletter.

Ready to learn the ropes? Dive into our SDIRA Rules Guide

2. Lean on Third-Party Professionals

It’s often a good idea to consult trusted professionals, such as tax advisors, legal counsel, or financial planners, who are well-versed in the SDIRA rules.

3. Choose a Reliable SDIRA Provider

Your SDIRA custodian is responsible for recordkeeping and timely reporting to the IRS. Select a provider with decades of experience offering the type of investments you’re considering. Work with a provider that offers ample resources and guidance, such as educational materials or a knowledgeable client services department.

4. Maintain Proper Documentation

Detailed recordkeeping is critical to proving that your IRA is compliant with IRS rules. While your SDIRA provider is the primary party responsible for recordkeeping, it’s a good idea to keep personal copies of all transactions, ownership documents, and financial agreements related to your SDIRA. Proper records can prove invaluable in the case of an audit by the IRS.

Self-Directed IRA Prohibited Transaction FAQs

Before we wrap up, here are some of the most commonly asked questions we receive about self-directed IRA prohibited transactions:

1. Why did I never hear about prohibited transactions when I invested with my brokerage?

All IRAs operate under the same rules, so it’s theoretically possible to commit a prohibited transaction with an IRA that is solely invested in publicly traded securities.

Though, in general, publicly traded securities do not pose a significant risk for prohibited transactions because they are transparent, liquid, and traded on regulated exchanges. These assets are standardized and values are determined by the market. You can’t easily manipulate the price of a stock or bond to benefit yourself or a disqualified person.

In contrast, alternative assets such as real estate, private loans, or private equity, can present greater risks for prohibited transactions. These assets are often less liquid and harder to value, which opens up more opportunities for misuse.

For example, an investor might be tempted to engage in self-dealing by purchasing an undervalued property from a relative or by using an IRA-owned asset for personal benefit, both of which would be considered prohibited transactions.

2. Can I manage a property held in my SDIRA?

You can oversee the management of the property but must stay at arm’s length. You cannot personally provide services (such as repairs or renovations) as this is considered self-dealing.

3. Can my SDIRA lend money to a disqualified person?

No, lending money to or borrowing from a disqualified person is a prohibited transaction, even if interest is paid back to the IRA.

4. Can my SDIRA invest in a business I own?

No, IRA holders cannot use their SDIRA to invest in their own business or a business owned by disqualified persons.

5. Can my SDIRA purchase an asset I already own?

No, your SDIRA cannot purchase assets that you, or any other disqualified persons, currently own.

6. Can I partner my IRA funds with disqualified persons?

Yes, but only at the time of initial purchase. After the investment is made, no transactions involving disqualified persons can occur, including commingling of funds.

7. Can I take a personal loan on the property owned by my IRA?

No, taking a personal loan using SDIRA-owned property as collateral is prohibited. However, the IRA can obtain a non-recourse loan, where the loan is secured solely by the IRA-owned asset.

Learn More About Self-Directed IRA Prohibited Transactions

By investing in your education, seeking professional advice, maintaining proper documentation, and working with a reputable provider, you can effectively avoid prohibited transactions and safeguard your SDIRA’s tax-advantaged status.

Want to learn more about the rules governing self-directed IRAs? Download our SDIRA Basics Guide. Inside, we’ve included a detailed breakdown of the key IRS rules to be aware of before opening an SDIRA.

And if you have more questions about prohibited transactions, you can talk to one of our SDIRA experts. They can give you the general information you need to navigate the IRS rules and protect the tax-advantaged status of your retirement portfolio.

0 Comment