Estimated reading time: 5 minutes

You are. That is, if you own a self-directed IRA (SDIRA).

A disqualified person is someone who is prohibited from engaging in certain types of transactions with an individual IRA.

The IRS created specific regulations to prevent self-dealing and ensure that IRAs are being used for their primary purpose – to make investments that provide income during retirement. After all, these funds were given privileged tax-exempt status. The IRS wants to make sure that status isn’t being exploited due to self-dealing or conflicts of interest.

So, engaging in transactions with disqualified persons can result in the immediate distribution of the entire IRA. This can lead to a potentially significant tax bill and a 10% early withdrawal penalty, if applicable.

In this article, we’ll cover the different types of disqualified persons, plus some all-too-common examples of transactions with disqualified persons to avoid.

Table of Contents

- Are All IRAs Subject to the Disqualified Persons Rule?

- Categories of Disqualified Persons

- Examples of Transactions with Disqualified Persons

- Consequences of Engaging with Disqualified Persons

- Familiarize Yourself with Disqualified Persons

Are All IRAs Subject to the Disqualified Persons Rule?

Yes, all IRAs are subject to the disqualified persons rule. However, the concept of "disqualified persons" and prohibited transactions primarily comes into play with SDIRAs because of the unique nature of the assets allowed within these accounts.

With most IRAs, you’re only able to invest in stocks, bonds, and mutual funds on the public markets. On open markets, the risk of self-dealing or other conflicts of interest is fairly negligible. Most can't influence the price of a publicly traded stock like Exxon or Microsoft to benefit themselves unfairly.

With an SDIRA, assets like real estate or private equity do not have readily available market prices, increasing the risk of transactions that could benefit the IRA holder or other disqualified persons unfairly.

For instance, IRAs were not granted their tax-exempt status to allow for IRA holders to buy a second home or rent an apartment to a grandchild at an affordable rate. That’s a significant conflict of interest.

That’s why the IRS has detailed rules to prevent self-dealing and ensure that retirement funds are used appropriately.

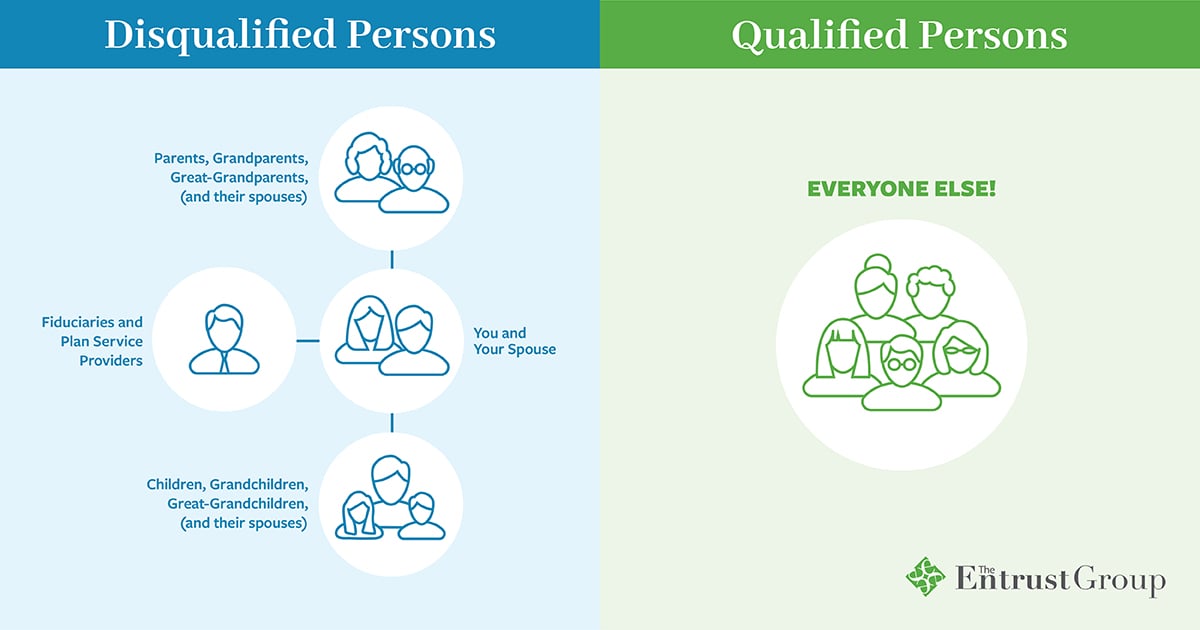

Categories of Disqualified Persons

There are four main types of disqualified persons:

The Account Holder and Their Spouse

The IRA owner and their spouse are automatically considered disqualified persons. This is because the IRS aims to prevent the IRA owner from using the funds for personal benefit before retirement. Any transaction between the IRA and the account holder or their spouse is strictly prohibited to avoid self-dealing.

Lineal Ascendants and Descendants

Lineal ascendants (e.g., parents, grandparents, great-grandparents, and their spouses) and descendants (e.g., children, grandchildren, great-grandchildren, and their spouses) of the IRA owner are also considered disqualified persons.

Fiduciaries and Advisors

Fiduciaries and advisors, or any person providing services to the IRA, fall under the category of disqualified persons. This includes anyone who has a fiduciary responsibility to the IRA, such as investment advisors, accountants, and attorneys. Their role involves managing or advising on the IRA’s investments, and any transaction between the IRA and these individuals could lead to conflicts of interest or self-dealing.

Entities Controlled by Disqualified Persons

Entities such as corporations, partnerships, trusts, and estates that are controlled by disqualified persons are also considered disqualified. Control is defined as owning 50% or more of the entity.

The reason for this disqualification is to prevent indirect self-dealing. For example, if the IRA invests in a corporation that is controlled by the IRA owner or their family, it could be seen as a way to indirectly benefit from tax-exempt IRA funds.

Examples of Transactions with Disqualified Persons

Here are three common prohibited transactions involving disqualified persons to avoid:

Real Estate Transactions

If an IRA owner attempts to sell a property they personally own to their IRA, or if the IRA purchases a property from a disqualified person (such as a parent or child), this transaction is prohibited. Similarly, the IRA cannot buy a property and then lease it to a disqualified person, as this constitutes indirect benefit.

Example: John owns a rental property personally and wants to sell it to his SDIRA for investment purposes. This transaction is prohibited because John, as the IRA owner, is a disqualified person. In theory, John could sell the property at an incredibly low price to his IRA, transferring wealth from his taxable accounts to his tax-advantaged accounts, unfairly reducing his tax liability.

Personal Use of IRA Assets

Any personal use of assets owned by the IRA by disqualified persons is strictly prohibited. For example, if the IRA owns a vacation property, neither the IRA owner nor any disqualified person (such as a spouse or child) can use it, even temporarily.

Example: Sarah’s SDIRA owns a vacation home. If Sarah, her spouse, or her children stay in the vacation home, even for a weekend, it constitutes a prohibited transaction. The property must be used strictly for investment purposes and cannot provide any personal benefit to disqualified persons.

Loans and Payments

Loans to or from disqualified persons are prohibited transactions. This includes any direct or indirect loans between the IRA and disqualified persons. Nor can an IRA holder use the IRA as collateral in order to secure a loan.

Example: Mark wants to use funds from his SDIRA to lend money to his own business. This is a prohibited transaction because Mark is a disqualified person, and the loan would constitute self-dealing. Similarly, if Mark uses his IRA funds to pay for personal expenses, this would also be prohibited.

Consequences of Engaging with Disqualified Persons

Engaging in transactions with disqualified persons can result in severe penalties and tax implications.

The most immediate consequence is the disqualification of the entire IRA on the first day of the tax year the transaction occurred.

For instance, if the IRS finds you engaged in a prohibited transaction with your SDIRA on December 17, 2024, the entire account is considered distributed on January 1, 2024. The tax-advantaged status of the entire account is lost. Thus, the entire value of the IRA may be subject to income tax and potential early withdrawal penalties.

Example: You are 50 years old and have a traditional IRA with a balance of $500,000. You decide to use the funds to purchase a rental property, and then rent the property to your daughter. This transaction is prohibited because your daughter is a disqualified person.

So, the entire value of the traditional IRA ($500,000) would be considered distributed on the first day of the tax year. If the entire IRA balance was tax-deferred, you would owe income taxes on the entire amount in the year of distribution.

For most taxpayers, this would lead to a single-year federal tax bill of over $160,000. If you live in a state with high income taxes, tack on another $30,000-$60,000. Plus, because you’re under the age of 59½, the $500,000 is subject to a 10% early withdrawal penalty, adding another $50,000 to your bill.

Finally, the IRS may impose a 15% additional excise tax on the amount involved in the prohibited transaction.

And there you have it – a significant portion of your IRA funds was just wiped out in one fell swoop. Hopefully this example illustrates the serious penalties facing those who transact with disqualified persons.

Familiarize Yourself with Disqualified Persons

Adhering to IRS rules is crucial to maintain the tax-advantaged status of an SDIRA. Compliance ensures that the investments grow tax-deferred or tax-free, depending on the type of IRA, and protects the IRA from severe penalties.

Engaging with qualified professionals can significantly reduce the risk of prohibited transactions. Consider consulting with trusted financial advisors and legal professionals who have the expertise to guide you through the complexities of SDIRA regulations.

Lastly, remember that the Internal Revenue Code isn’t carved in stone. The rules often change from year to year. Subscribe to our monthly newsletter to stay informed about any updates or changes in regulations that may affect your IRA.

26 Comments